I don't think it's that simple. As with any market, it's not just the seller that determines the price. Banks weren't forcing this down investors' throats. In addition, banks weren't just selling this stuff - they were buying it too.

Well, yeah. Banks are active on the supply and demand side -- they were packaging risk up for sale an buying it on the cheap. And because banks are banks, even when they're not commercial and not regulated by the central bank, as we've seen, they're still too valuable to be allowed to fall. Banks operate on the pretense of investive security, but in reality all financial activity is uncertain and risky and the point NNT makes is that the more you think you have your risk covered with derivatives and other hedges (or whatever), the more you mistake the unlikely for the impossible and the more likely that when the unexpected happens, it will be a disaster.

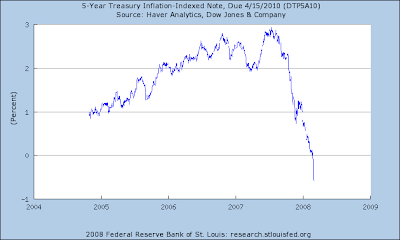

For another, although the risk associated with the riskier slices of subprime mortgage securities was definitely mispriced (by lenders, investors and rating agencies), I'm less convinced that the risk associated with senior and super-senior debt was off - like I said, actual defaults still haven't eaten into a lot of this paper. But because everyone's terrified that losses will emerge there, no-one's willing to buy it. The market as a whole has effectively repriced the risk, and the pendulum may well have swung too far the other way - but banks are the only ones who have to recognise this repricing by reporting it as a loss.

Of course, I think that's exactly right and in line with the stuff I've been linking to. Debt per se if definitely not the problem as I see it. The shitty CDO debt was a problem, and while everyone figures out who owns what, it will remain a problem to some extent. This really points to solvency, not liquidity (although liquidity

was a problem, I don't see how liquidity can be a problem anymore. For instance, the Fed is currently

draining US banking reserves to counter excess liquidity), in that no one knows who's going to be holding what when the music stops.

I agree that prime mortgages and senior debt was probably fairly priced. Even the sub-prime "bad debts" will get repackaged up and sold onto someone else who can try to extract some value from them. I don't think that banking or usury is the problem, and I don't want to do banks' jobs for them. The problem is really confusing uncertainty with risk, and not being able to recognise when your 25-sigma movements are not really 25-sigma at all. Then it becomes an issue of trust and, again, uncertainty.

That's right. Is it good regulation, though?

Almost certainly not, and that's probably unsuprising. Be interesting to see what happens next. The SEC have been pretty quiet, and I guess that the investment banks are the Fed's responsibility now.